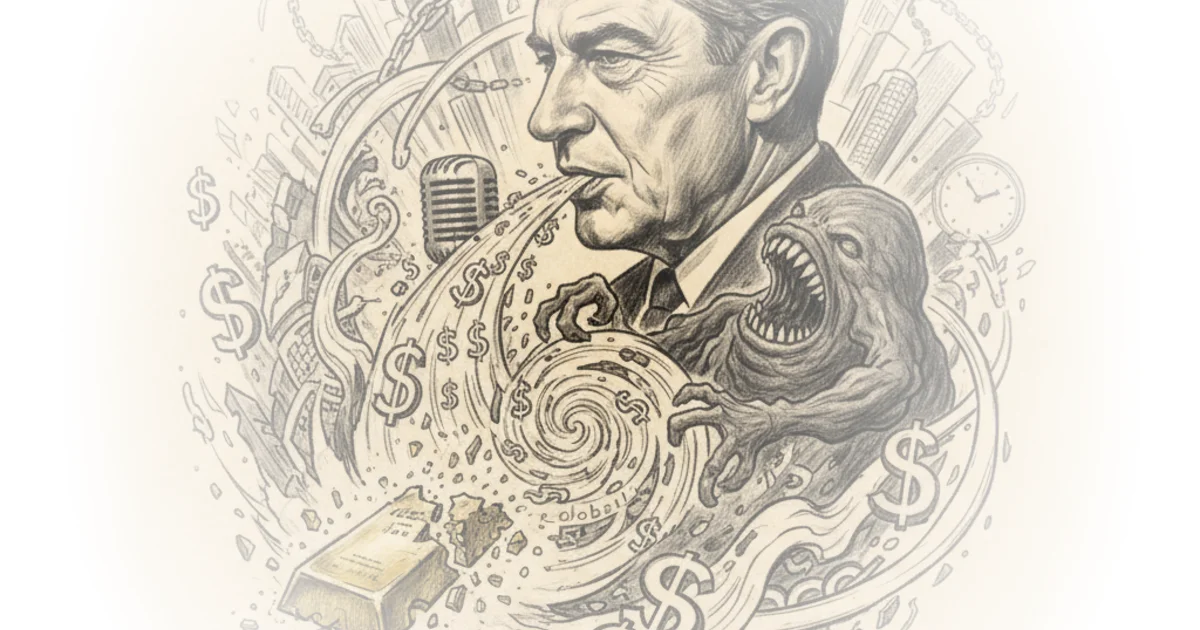

The World Owes Money to Itself

Caspian Report's Shirvan presents a sweeping history of global debt, tracing the arc from grain loans between neighbors to a $345 trillion web of obligations that now constitutes the operating system of the modern economy. The thesis is provocative and cleanly stated: debt is no longer a tool used by the system. It is the system. And the video's central paradox deserves serious attention.

If everyone owes money to everyone else, then who is all that money actually going to? The answer isn't what you think. Follow the money far enough, and the trail circles back to where it started. The world essentially owes money to itself, and it works so long as no one checks the math.

That framing is vivid and largely accurate as a description of sovereign debt mechanics. The circular flow between domestic savers, banks, pension funds, and government treasuries does create a closed loop in which money cycles from lender to borrower and back again. The international version scales the same pattern: Japanese savings fund Saudi projects, Saudi capital flows to Brazil, Brazilian money buys American bonds. Shirvan is right that the architecture is self-referential. But the implication that nobody is "checking the math" understates the enormous apparatus of bond markets, credit rating agencies, and central bank surveillance that exists precisely to do that checking in real time.

Nixon and the Gold Standard: Necessary Context

The video anchors its narrative on August 15, 1971, when Nixon severed the dollar's convertibility to gold. This is standard monetary history, and Shirvan handles it competently, connecting the Bretton Woods system's constraints to the pressures of Vietnam-era spending. The move to fiat currency did indeed remove the physical ceiling on money creation.

From that point forward, governments gained the ability to create money at will. And with the old restraints gone, a new system emerged where debt could expand as long as lenders remained confident in government decrees.

What goes unmentioned is that the gold standard had its own severe pathologies. The interwar gold standard contributed directly to the Great Depression by forcing countries into deflationary spirals. Economists like Barry Eichengreen have argued persuasively that the gold standard was not a neutral anchor but an active constraint that amplified downturns. The shift to fiat currency was not simply a removal of discipline; it was also a removal of a mechanism that had repeatedly caused catastrophic economic contractions. The video's framing implies a lost golden age of fiscal restraint that never quite existed.

The Debt-as-Engine Argument

Shirvan's strongest section explains how government borrowing functions as an economic engine. The description of COVID-era spending is particularly effective.

In America, the government borrowed $3.1 trillion in a single year, which was about 12% of the economy at the time. China, Europe, and every other major economy did the same. It wasn't a choice really. It was necessity.

This is well-stated and reflects mainstream economic consensus. When private spending collapses, government borrowing fills the gap. The alternative, as demonstrated by austerity programs in Greece and elsewhere during the 2010s, tends to be prolonged recession and social instability. The video correctly identifies that modern economies are structurally dependent on continuous borrowing.

However, the analysis would benefit from distinguishing between types of debt. Not all government borrowing is equivalent. Debt incurred to build infrastructure, fund education, or invest in research generates future economic returns that can exceed the cost of borrowing. Debt used to finance tax cuts for high earners or to service existing interest payments does not carry the same productive potential. The $345 trillion headline figure mixes productive investment with pure financial engineering, and treating them as a single phenomenon obscures more than it reveals.

The Developing World Gets Short-Changed

The video briefly acknowledges that the debt cycle works differently for wealthy nations than for developing ones. Germany and Switzerland borrow cheaply; Kenya and Pakistan are trapped. But this disparity deserves far more attention than it receives. The international debt architecture is not a neutral playing field. Developing nations often borrow in dollars or euros, meaning that currency fluctuations can dramatically increase their repayment burden through no fault of their own fiscal management.

Countries like Kenya and Pakistan, for instance, are stuck in debt traps and forced to keep borrowing just to meet interest payments on past loans. So, the same debt that strengthens some economies can end up holding others back.

Economists like Jayati Ghosh and the United Nations Conference on Trade and Development have argued that the current system amounts to a structural transfer of wealth from the Global South to the Global North. When Shirvan says "the world owes money to itself," the "itself" obscures massive asymmetries. The world owes money to specific institutions, in specific currencies, under specific legal frameworks that overwhelmingly favor creditor nations. A Zambian farmer and a Wall Street bondholder are not equal participants in this loop.

The Missing Players

One notable absence from the analysis is the role of private debt. The $345 trillion figure includes household mortgages, corporate bonds, and financial sector leverage, not just government borrowing. Yet the video focuses almost exclusively on sovereign debt. In many crises, including the 2008 financial collapse, it was private debt that proved most dangerous. Overleveraged banks and mortgage-backed securities nearly destroyed the global financial system, and governments took on enormous public debt precisely to bail out private actors. The relationship between public and private debt is far more complex than the video suggests.

Central banks also receive surprisingly thin treatment. The discussion of quantitative easing is reduced to "printing money causes inflation," which is a significant oversimplification. The Bank of Japan has pursued aggressive quantitative easing for decades without triggering runaway inflation. The European Central Bank's bond-buying programs stabilized the eurozone. The relationship between money supply expansion and inflation depends heavily on context, including labor market conditions, supply chains, and global commodity prices. The Zimbabwe example, while dramatic, is an extreme outlier driven by agricultural collapse and political dysfunction, not merely by printing money.

Perpetual Motion and the Physics Metaphor

The video closes with a dramatic comparison.

This perpetual motion, however, can't keep going forever. Eventually, there will be a reckoning, an economic depression. Centuries ago, physics proved that perpetual motion is impossible. Economics is yet to come around.

It is a memorable line, but the physics analogy is misleading. Economies are not closed thermodynamic systems. They can grow through innovation, population change, and productivity gains. Debt sustainability depends not on whether debt exists, but on the ratio of debt service costs to economic output and the productivity of the investments that debt finances. Japan carries a debt-to-GDP ratio exceeding 250 percent and has done so for years without crisis, because its debt is overwhelmingly domestically held and denominated in its own currency. The "inevitable reckoning" framing makes for compelling television but represents only one school of economic thought, and not the dominant one among central bankers and fiscal economists.

Bottom Line

Caspian Report delivers an accessible and well-paced overview of how global debt evolved from personal promises to a $345 trillion architecture that underpins modern civilization. Shirvan's central insight, that the system is circular and self-reinforcing, is valid and important for a general audience to understand. Where the analysis falls short is in its treatment of asymmetries between wealthy and developing nations, its neglect of private debt's role in systemic crises, and its reliance on a physics metaphor that implies inevitable collapse rather than the more nuanced reality of ongoing management and periodic restructuring. The global debt system is not a perpetual motion machine heading for a wall. It is a complex, unevenly distributed, continuously negotiated set of relationships, and its future depends far more on political choices than on thermodynamic inevitability.